Tariffs happened, and then most were paused. By now, if you’re like me, you’ve received a dozen newsletters or articles detailing the specifics of the tariffs. So I’ll spare you more of those details.

What I want to focus on here is what else beyond tariffs we should be paying attention to this month.

JOC published an excellent article on April 8th that said:

“Expectations that the domestic truckload market would turn upward by mid- or even late 2025 are fading as US tariffs rattle freight markets After an uptick in the first quarter, truckload pricing is returning to depressed levels close to the bottom it first struck in 2023, third-party logistics provider AFS Logistics said Tuesday in its second-quarter TD Cowen/AFS Freight Index Forecast.”

And then, on April 9th, Trump put a 90-day pause on almost all tariffs, with China being the exception.

Where does that leave us now? Well, it might mean most people resume business as usual, knowing they have at least 90 more days before things get dicey again. I’d expect if negotiations aren’t complete by day 60 with any countries BCOs are pulling goods in from, we might start seeing some pull-forward show up in bookings.

Until then, it seems navigating tariffs, and retaliatory tariffs with China, will be supply chain decision makers’ primary concern.

I’ve written and re-written this report several times over the past few days. And because of that, I’ll spend no more time digging into tariffs themselves, and instead focus, as usual, on economic data and freight market updates that are helpful regardless of any changes in tariff activity over the next month.

JP Morgan increased the likelihood of a recession from 40% to 60% in the last week, and despite the 90 day pause yesterday, they have refused to downgrade that estimate again. For obvious reasons, this has a lot of people rightfully concerned.

“But economists and analysts warned that despite Wednesday's rally, the market will likely experience continued volatility because of lingering uncertainty about Trump's endgame and whether the U.S.-China trade war will escalate.”

However, the White House disagrees.

““I see no reason that we have to price in a recession,” Bessent told NBC’s Meet the Press with Kristen Welker, despite economists at JPMorgan saying Friday they now expect the US to slip into a recession this year.”

I have been diligently covering the makings of a “soft landing” for almost 2 years now in this newsletter, and I have to admit that complete tariff chaos was not on my bingo card. I’m still trying to sift through ungodly amounts of news articles to try to make sense of what is actually worth paying attention to right now. But, the basics don’t change. So let’s review some key economic drivers of the full truckload freight market.

Jason Miller , Eli Broad Professor of Supply Chain Management at MSU, provided these graphs with the following commentary:

“Both the Federal Reserve Banks' Manufacturing Surveys as well as ISM have shown a sharp downturn in the momentum for new orders, which had shown substantial improvement in January. Both were strongly negative in March. In total, ISM is capturing about 400 firms, whereas the Fed Banks are capturing about 500 firms from their respective districts.”

Both the Fed Banks and ISM are showing sharp upward increases in the prices paid for inputs (see below). It is quite odd to see the combination of declining orders but upward pricing pressure for materials.

The Institute for Supply Management said alongside the PMI release that

“Fiore continues, “In March, U.S. manufacturing activity slipped into contraction after expanding only marginally in February. The expansion in both February and January followed 26 consecutive months of contraction. Demand and output weakened while input strengthened further, a negative for economic growth. Indications that demand weakened include: the (1) New Orders Index falling further into contraction territory, (2) New Export Orders Index dropping into contraction, (3) Backlog of Orders Index contracting at a faster rate, and (4) Customers’ Inventories Index remaining in ‘too low’ territory. Output (measured by the Production and Employment indexes) also weakened. Factory output (production) contracted in March, indicating that panelists’ companies are revising production plans downward in the face of economic headwinds… Inventories growth is a temporary move to avoid tariffs and will decline when such trade issues are resolved. Demand and production retreated and destaffing continued, as panelists’ companies responded to demand confusion. Prices growth accelerated due to tariffs, causing new order placement backlogs, supplier delivery slowdowns and manufacturing inventory growth.”

I suspect there has been enough uncertainty around tariffs over the last 60 days, and now still quite a bit for the next 90, that a “wait and see” or “proceed with caution” approach is going to be widely adopted across manufacturers.

However, manufacturing tends to follow consumer demand, which has stayed strong for years. I don’t expect spending to increase, but if we can at least hold steady at or near current levels, there’s a chance manufacturing avoids slipping further.

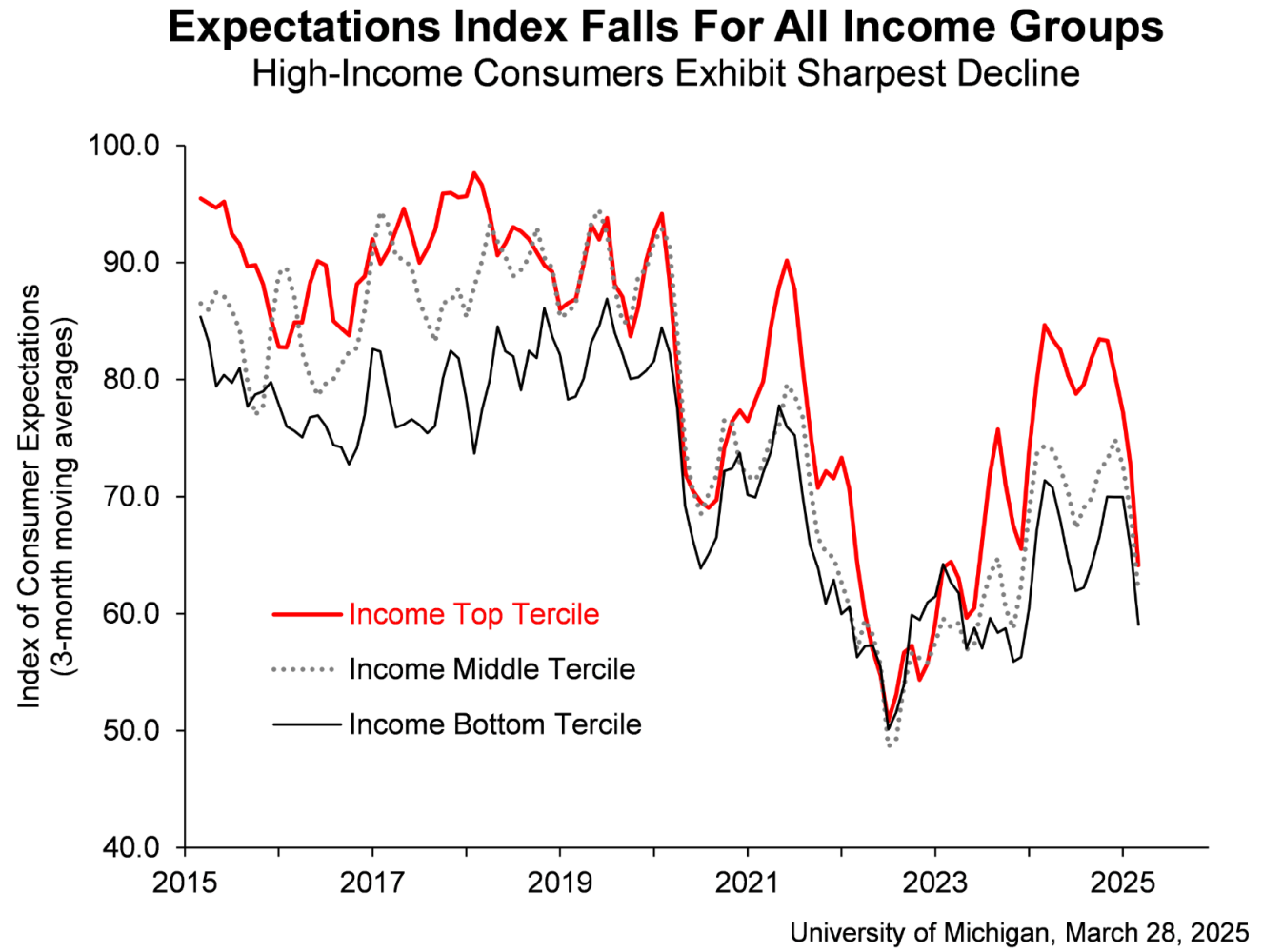

Unfortunately, consumer sentiment registered a pretty bad low in March.

Consumer confidence dropped again in March, marking the third straight month of declines. The expectations index fell 18 percent, and overall sentiment is down 12 percent from February. People across political lines all reported a more negative outlook when it comes to their personal finances, inflation, the job market, and general business conditions.

Two-thirds of consumers now expect unemployment to rise in the next year. That is the highest level we've seen since 2009. It matters because a strong job market has been one of the few things keeping consumer spending steady lately.

Inflation expectations also jumped. Short-term inflation is now expected to hit 5 percent, up from 4.3 percent last month. That’s the third month in a row we’ve seen a sharp increase. Long-term inflation expectations moved up too, mainly driven by independents. This reflects a broader sense of concern. What remains to be seen now is how much of this sentiment will end up becoming hard data in the near future. In other words, will peoples’ feelings be enough to alter behaviors in a meaningful way.

Wage growth, which we will unpack in a minute, is still positive. The March jobs data showed cracks, but was not showing signs of impending disaster yet. Something we have looked at in this report before is the Personal Savings Rate. The personal savings rate is the % of disposable income that consumers are saving each month. The savings rate increased, and it will be interesting to see if that continues for the next several months. It might be that consumers, concerned about the uncertainty in the market, are shifting their dollars from spending to savings. Uncertainty tends to make the average household more cautious. However, the fact that people are increasing their savings at all right now, reversing a decline trend in savings throughout the recent inflationary years, is probably still a positive.

The most recent data we have on consumer spending and savings (updated through Feb) shows:

"Personal income increased $194.7 billion (0.8 percent at a monthly rate) in February, according to estimates released today by the U.S. Bureau of Economic Analysis. Disposable personal income (DPI)—personal income less personal current taxes—increased $191.6 billion (0.9 percent) and personal consumption expenditures (PCE) increased $87.8 billion (0.4 percent).

Personal outlays—the sum of PCE, personal interest payments, and personal current transfer payments—increased $118.4 billion in February. Personal saving was $1.02 trillion in February and the personal saving rate—personal saving as a percentage of disposable personal income—was 4.6 percent."

And while consumer sentiment is poor, the White House again takes a positive stance.

“Kevin Hassett, head of the White House’s National Economic Council, acknowledged that US consumer prices “might go up some” as a result of Trump’s tariffs, but suggested that concern among economists, the Federal Reserve and some lawmakers was overblown. Speaking on ABC’s This Week, Hassett said he doesn’t anticipate “a big effect on the consumer in the US” and that Americans will eventually benefit from tax and spending cuts that Trump wants to push through Congress.”

I find that last sentence to be the most interesting. I am not getting too deep into it today, but I found several sources estimating the overall financial impact of tariffs (the original tariff announcement) on US households. The estimations varied from $694-3,500/yr increase in household expenses. We don’t have details yet on what the “tax and spending cuts that Trump wants to push through Congress” might be, but some that have been proposed previously would seemingly offset some or all of this increased household burden. It’s difficult for consumers to gauge their appropriate level of concern when they don’t have all of the information. There’s definitely a tax to uncertainty. In freight terms, I remember when I was in LTL sales, when a customer asked me to bid an RFP and did not provide me with specifics of the materials moving, my team had to guess in order to run pricing models. Anytime you are guessing with financial impacts, you err on the side of caution. Understandably, businesses and consumers alike are erroring on the side of caution right now.

We need to be paying attention to two things right now as we try to understand what decisions the FED might consider making - wage growth and unemployment rates. Wage growth has fueled inflation, and low unemployment rates have been a demotivator to cut interest rates for fear of fanning inflation unnecessarily. Wage growth has been slowing the last several months, which is actually a good thing, although not enough to match a 2% inflation rate long term.

As always, Jan J. J. Groen did a great job summarizing the March jobs data.

The chart above shows that the increase in the job-finding rate led to a decline in the monthly flow-consistent unemployment rate for February into March. Given the choppiness in this measure, it’s probably more useful to look at three-month averages. Throughout most of 2024 the flow-consistent unemployment rate on a three-month average basis had been outpacing the official unemployment rate and leading the rise in the latter (solid blue and orange lines in the chart above). This was largely driven by a deterioration in the job finding rate over that period, which reflected labor demand weakening. More recently, three-month averages of headline and flow-consistent unemployment rates suggest that over the near term the unemployment rate will likely remain relatively stable around 4.2%. Both smoothed payrolls growth trends and the job lows data continue to show signs that the labor market remained stable and close to its underlying equilibrium.

His take is certainly more reassuring than consumer sentiment regarding unemployment, and I hope he is right. Jan also added,

Compared to both the composition-adjusted AHE data for production and non-supervisory workers for February and the unsmoothed Atlanta Fed wage tracker into January, annual wage growth rates still outpace the 2.75% pace consistent with 2% PCE inflation in the medium term (green line in the above chart). Current wage growth runs more closely in line with the wage growth pace consistent with 3.4% PCE inflation implied by “Main Street” near-term inflation expectations for March (blue line in the chart above).

I don’t envy the FED right now. Their job is growing increasingly more complex at the moment. Tariffs are threatening to add (and some have already added) inflationary pressures, while we are beginning to see potential cracks in our labor market and consumer sentiment expects unemployment to rise.

Along with most of the country right now, they seem to be settling into their “wait and see” approach. Gregory Draco wrote in a recent article of his that -

Unlike in 2024, when Federal Reserve officials were trying to ensure a soft-landing by easing policy to sustain a strong economy and accommodate favorable inflation developments, policymakers seem more focused on downside risks in 2025. But there are two camps. The first is more focused on downside risks to the economy. And the other more focused on upside risks to inflation. Powell sits in the middle awaiting greater clarity amidst elevated policy uncertainty. The Fed is—and will remain—highly reactive, leaning heavily on incoming data. This reactive stance supports holding rates steady through mid-year, with a potential tilt toward more aggressive easing in the second half of the year as the economy edges toward a recession.

Phil Rosen also added commentary on the Fed’s decision by saying-

Here’s Powell’s problem. If the latest jobs data confirms cracks in the labor market, Powell could be seen as negligent for doing nothing. But cutting while inflation expectations are rising also undermines the Fed’s credibility and threatens long-term price stability.

In speaking with Paul Poziumschi, Chief Economist at Transfix this month he provided that-

“Unsurprisingly, the ensuing volatility and disruption has led to recession risks to be revised upward, and tariff-driven inflation may constrain the Federal Reserve’s ability to respond if those risks materialize.”

Paul also added that

“In short, under most scenarios, some degree of short-term pain seems unavoidable.”

Short term pain sounds like something we can likely manage, adjust through, and recover from fairly quickly. Let’s hope that is the path forward.

I’ve grown increasingly frustrated with the coverage around tariffs and policy that claims there is “no plan” or “no intelligence.” Let’s be a little more mature than that. Of course there is a plan — many just happen to disagree with the logic behind it.

Regardless of where you stand, I still believe it’s our responsibility to understand the reasoning behind the decisions being made so we can be better prepared.

I have not yet completed my reading of this 41 page document and gathered my thoughts, but I felt it was timely to share with any others who might endeavor to read it. Reading things that make us ask questions, and even criticize, will often lead us to search for answers, which is a good thing!

One of Trump’s primary economic advisors, Stephen Miran, the chairman of the White House Council of Economic Advisers, published a paper (click here for paper) in November of 2024, its 41 pages and worth the read. He opens the paper by saying:

“The desire to reform the global trading system and put American industry on fairer ground vis-à-vis the rest of the world has been a consistent theme for President Trump for decades. We may be on the cusp of generational change in the international trade and financial systems.The root of the economic imbalances lies in persistent dollar overvaluation that prevents the balancing of international trade, and this overvaluation is driven by inelastic demand for reserve assets. As global GDP grows, it becomes increasingly burdensome for the United States to finance the provision of reserve assets and the defense umbrella, as the manufacturing and tradeable sectors bear the brunt of the costs.In this essay I attempt to catalogue some of the available tools for reshaping these systems, the tradeoffs that accompany the use of those tools, and policy options for minimizing side effects. This is not policy advocacy, but an attempt to understand the financial market consequences of potential significant changes in trade or financial policy. Tariffs provide revenue, and if offset by currency adjustments, present minimal inflationary or otherwise adverse side effects, consistent with the experience in 2018-2019. While currency offset can inhibit adjustments to trade flows, it suggests that tariffs are ultimately financed by the tariffed nation, whose real purchasing power and wealth decline, and that the revenue raised improves burden sharing for reserve asset provision. Tariffs will likely be implemented in a manner deeply intertwined with national security concerns, and I discuss a variety of possible implementation schemes.I also discuss optimal tariff rates in the context of the rest of the U.S. taxation system. Currency policy aimed at correcting the undervaluation of other nations’ currencies brings an entirely different set of tradeoffs and potential implications. Historically, the United States has pursued multilateral approaches to currency adjustments. While many analysts believe there are no tools available to unilaterally address currency misvaluation, that is not true. I describe some potential avenues for both multilateral and unilateral currency adjustment strategies, as well as means of mitigating unwanted side effects. Finally, I discuss a variety of financial market consequences of these policy tools, and possible sequencing."

Sounds like an interesting read to me.

A huge thank you to BiggerPicture for sponsoring this month's newsletter! BiggerPicture is focused on helping shippers, brokers, and carriers maximize their operational productivity, by reducing the time spent scheduling appointments by an average of 80%. Achieve full ROI in 3 months or less, and unlock new growth potential by shifting your most valuable resources (your peoples' time) where it can make the biggest impact.

I don’t typically include ocean rates or bookings in my newsletter, but since imports do have some impact on domestic trucking volumes, I wanted to take a brief glance this way in light of the heavy tariffs between the US and China. At the time of publication the latest update I have on imports from Asia, courtesy of JOC, is-

“Cargo bookings on vessels leaving Asia bound for the US over the next few weeks have fallen 20% to 30% as retailers delay the receipt of non-critical freight in the aftermath of the widespread global tariffs implemented by the Trump administration, sources tell the Journal of Commerce. And the chilling effect of the tariffs is extending further down the calendar, with forwarders in the trans-Pacific saying US retailers are holding off making purchase orders with factories in Asia for fall and holiday merchandise for 30 to 60 days.”

Some digging into recent import volumes has shown that there was a pull forward effort for imports all the way up to the April deadline.

And the impact of this pull forward on spot rates already seems evident. FTR’s most recent insights say:

Broker-posted spot rates in the Truckstop system rose for all equipment types for a second straight week during the week ended April 4 (week 13), and the gains were particularly notable for the van segments. The spot rate increases for both dry van and refrigerated were their largest of the year so far, and both saw back-to-back weekly increases for the first time since the start of the year. Flatbed spot rates rose for an eighth straight week and were at their highest level since June 2023. The sources of the recent strength in dry van and refrigerated and the ongoing strength in flatbed are unclear. We have suspected based on the geography and timing of the flatbed growth in volume that it could be tied to imports of equipment and metals in order to avoid impending tariffs. Dry van and refrigerated had not really seen any firming until a couple of weeks ago. However, it’s possible that this activity, too, could be linked to a pull-forward due to expectations, which proved to be correct, that broad-based import tariffs would be imposed in early April.

In addition to tariff impacts on freight volumes and rates, I also remembered that it’s transition time for produce. I checked in with my friend Cody Koehler of A&Z Trucking, one of the largest produce brokerages in the nation, with facilities in both Yuma and Salinas, to see how the transition was going. Cody said

“The Yuma to Salinas transition is underway in the West. The next few weeks will be messy with some shippers moving earlier than others. We often see a lot of split loading for several weeks with some lingering product still in Yuma. The forecast for the Salinas season has been a mixed bag. Forecasted demand is lagging due to ongoing uncertainty in the economy. Harvest numbers look solid compared to the last few years with no major water issues this spring in the Salinas valley. Cross border produce looks to be impacted by the new tariffs. 80% of avocados sold in the US come from Mexico, expected impact to avocado pricing is between 10-25%.”

And as always, here are the graphs we check on a monthly basis to track spot and contract rate movement in reefer and dry van, thanks to Ken Adamo and team at DAT Freight & Analytics.

There is still a pretty large gap between spot and contract rates, as of 4/1 dry van spot rates had fallen, but made some recovery in recent days amidst the tariff chaos.

Reefer rates so far this year are a very similar story.

Normal seasonality has returned to the full truckload freight market as supply (carriers) and demand (truckload volumes) seems to have reached equilibrium. JOC wrote recently that-

“US employment data for February revealed a larger-than-expected shortfall in trucking employment, throwing light on a structural change in the US trucking market. The shortfall implies that truckload capacity — at least at larger carriers — could tighten more quickly when demand rises. It also underscores a shift in employment and resources from larger carriers to smaller trucking firms, a shift that may be permanent. That has implications for shippers and freight brokers planning for 2025 and beyond.”

That's all for this month!

Meet Me For Coffee with Samantha Jones seeks to correlate macro-economics to freight markets (just like this Newsletter does) and offers a chance to hear various industry and non-industry experts explain their thoughts on economics and freight markets.

Check out our Channels on your preferred platforms!

Thank you so much for reading and supporting the Truckload Market Update Report, produced by Samantha Jones Consulting LLC. Samantha Jones Consulting focuses on helping companies in the logistics industry better brand and sell their services to create sustainable revenue growth, and support their company growth goals!

We love Feedback, if you have questions, comments, suggestions, or are interested in sponsorships or partnerships, please email samantha@connectsjc.com to connect!

Make sure you subscribe to the Newsletter to receive the monthly update, and please share this with a friend who can also benefit from reading! As always, Samantha's work is free and created with the intent to add value to the transportation industry.