Had I written this report any earlier my information would have already been dated, and there’s a very real possibility it will be by the time I publish in two days. Tariffs have been in the spotlight as the initial tariffs promised went into effect on March 4th, however there have been further delays and amendments to these tariff policies since then. I will do my best to provide a succinct but comprehensive enough overview in this month’s report. In addition to tariffs and some of the usual economic data sources I frequently discuss (PMI, Jobs Data, etc) I couldn’t turn down the chance to cover a couple of the rabbit holes I found myself running down this month in absolute fascination. Those being: AI’s impending takeover, and the $28B of gold bars that were imported into the US in January👀.

Markets don’t like uncertainty, and we are definitely lacking certainty regarding tariffs. That is why we saw stocks in the United States closed down 1.8 percent on Thursday, March 6th. Just two days after imposing sweeping tariffs on Canada and Mexico, President Trump abruptly suspended many of them, leaving investors and businesses scrambling. He announced that products traded under the U.S.-Mexico-Canada Agreement (USMCA) would be exempt from the 25% tariffs he had just put in place, effectively walking back a significant portion of the levies meant to curb drug and migrant flows. This reversal came after automakers warned the tariffs would severely impact U.S. car production. While they were granted a 30-day reprieve, Trump suggested more tariffs on Canadian and Mexican goods are still on the way in April.

I would say there’s still enough uncertainty around when additional tariffs could come into play, when current ones might be changed, and to what extent. So for the sake of publishing something more useful amidst these changes I want to focus on two things: what industries and goods are most impacted, and what the broader economic implications of tariffs could mean. As a starting point, The US imported about $413b worth of goods from Canada, $505b from Mexico and $440b from China in 2024.

I found the above chart to be particularly helpful. After digging deeper into China, Mexico and Canada tariffs, here were my most up to date high level take aways:

Here’s the deal. Statements made by both President Trump and the Treasury Secretary Scott Bessent seem to acknowledge this one important fact that I am seeing covered minimally:

“Trade accounts for about a quarter of U.S. economic activity, compared with roughly 70 percent for Mexico and Canada. Canada and Mexico both send about 80 percent of their exports to the United States, while only about a third of U.S. exports go to Canada and Mexico collectively."

In other words, Canada and Mexico simply cannot cut ties with the US, and it will force negotiations. While Trump has loudly used tariffs to crack down on fentanyl and illegal immigration, that is not the primary driving force behind these tariffs it seems. I say that because there has been tremendous progress shown in recent months on curbing the trafficking of fentanyl and in illegal immigration. In addition, Canada is said to be responsible for less than 1% of fentanyl that makes it into the US. So what is the reason? Commentary by Treasury Secretary Scott Bessent covered in the NY Times seems to be more illuminating in this regard:

“Mr. Trump’s economic advisers have argued that the tariffs will not fuel inflation. However, Treasury Secretary Scott Bessent acknowledged on Thursday that there could be a temporary uptick in prices. “Can tariffs be a one-time price adjustment? Yes,” Mr. Bessent said at the Economic Club of New York. But Mr. Bessent said that as part of Mr. Trump’s broader economic agenda, which includes increasing energy production and rolling back regulations, he was not concerned about trade policies leading to higher prices. “Across a continuum, I’m not worried about inflation,” Mr. Bessent said.”

I went digging into this commentary deeper and found this information helpful to try to grapple with the “why” behind all the disruption. I listened to an interview Mr Bessent had with CNBC, and here were some notable callouts, although the entire interview is worth a listen.

Bessent claimed that the economy has become “hooked” on high levels of government spending that is not healthily sustainable. He likened their changing policies to a detox period. Where, there will be an initial shock period, but then ultimately things will be better off for it.

“It’s a much needed course adjustment…Could we be seeing that this economy that we inherited is starting to roll a bit? Sure. And look, there’s going to be a natural adjustment as we move away from public spending to private spending,” Bessent said on CNBC’s “Squawk Box.”

“The market and the economy have just become hooked. We’ve become addicted to this government spending, and there’s going to be a detox period,” he added. “I’m confident if we have the right policies it will be a very smooth transition”

“What we are trying to do is make free trade, fair trade, the trading systems have become incredibly imbalanced, you see it with these gigantic deficits that we run, you see it with the surpluses that other countries are accumulating. So we are going through, we are looking at tariff barriers, non-tariff barriers, currency manipulation, government subsidies. And in the EU some of these gigantic fines they are putting on our tech companies just because they see a big pool of capital. And we are going to push back on those… We are going to put this at the feet of our trading partners on April 2nd.. And it will be a choice, either they can drop the market manipulation that has hurt American workers. And if they do that, then we can have more frictionless trade, or we will put up the tariff wall, we will collect a lot of money, and we will make the system fair.”

I'll circle back shortly to more thoughts as to why Bessent and others seem comfortable with some economic slowdown and temporary shock to markets.

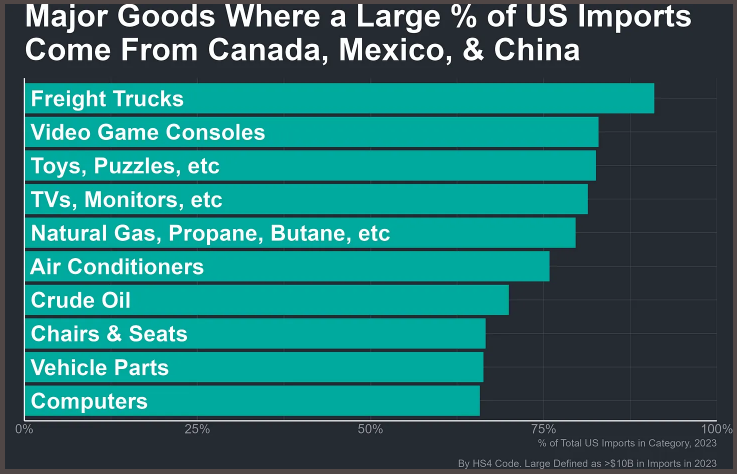

For a high level snap shot of goods most relevant to the tariffs conversation, American economist Joseph Politano has supplied these graphs:

For a very detailed breakdown of what percentage of over 150 commodities we import come from Mexico, China and Canada, check the following article that used the full year 2023 trade data.

As mentioned, markets do not like uncertainty. There are a lot of emotions right now, and a lot of indices and surveys depend on how people, consumers, employees, and businesses “feel” about the future. These feelings are considered and often influence actions, but to a lesser degree than underlying facts and reality influence the markets.

Sources like the U.S. “Economic Policy Uncertainty” estimated by the economists Scott R. Baker, Nick Bloom, and Steve Davis that relies on news articles, professional forecasters’ disagreements and other sources have been very negative in regards to the current feelings that are influencing surveys, articles, and media coverage of the US economy. With so much rapid volatility, that is no shock. It’s a little soon to call yet if these types of measurements will also show up in hard economic data to be equally as negative. As Matthew Klein wrote on this topic in The Overshoot:

“So far, the market action has been relatively modest compared to what is implied by some of the surveys or the policy uncertainty indices. Traders may be betting that behavior will change, or they may not be fully pricing in the risks associated with persistent policy volatility. If most of the damage cumulates slowly, people with higher discount rates may simply not care to the extent that the near-term outlook is less affected. Moreover, there have not yet been any legislative changes to taxes or spending, which could potentially offset—or exacerbate—some of the unwelcome impulses to growth and inflation associated with executive branch policy volatility.”

Another independent American Economist, Kyla Scanlon , had mentioned commentary made by Bessent in her recent publication that caught my eye during research. Her article made the observation that the current administration seems to be fully aware that they are intentionally slowing down the US economy. Additional conversations from Bessent she cited said:

Treasury Secretary Scott Bessent, who really wants 10Y yields to go down and is focused on increasing the ‘desirability’ of Treasuries (which is a sign of slowing economic growth expectations), said this on CNBC when asked about the potential of a recession: We're going to reprivatize the economy and as we bring down government spending and get the private sector moving again. That may not be a perfect one to one ratio. He then added that when asked when it becomes "Trump's economy," the President said: "probably six or twelve months out. I think I would agree with that."

In addition, she cited the US Secretary of Commerce, Howard Lutnick:

“the Trump administration would balance the federal budget with spending cuts, saying that would help growth and reduce the interest rates paid by consumers. He ended with “This is going to be the best economy anybody’s ever seen. And to bet against it is foolish.” So, there is some sort of plan here.”

Okay, now let’s entertain ourselves with a couple of my rabbit holes.

Kyla detailed an entire potential theory on the current economic policy disruptions being groundwork to allow the government and the US economy to be prepared to rapidly adopt AI as the economy surges back into a position of productivity and strength. Bessent also mentioned the current administration's unhappiness with Europe’s fines on our tech companies, it sent me exploring the concept of AI. And let me tell you, what I found is a theory I’m eager to follow. I cannot possibly write a comprehensive enough paragraph on this topic, so I encourage you to read the following article or listen to the interview.

To summarize as best as I can, it seems almost all AI labs and experts are in agreement that A.G.I. is coming quickly, like 6 months quick and definitely major changes in the next 2-3 years. This particular interview is between Ezra Klein, a columnist for the NY Times, and Ben Buchanan, the Biden administration’s A.I. advisor.

While I write this article myself, I had to use AI to summarize this long discussion as best I could. I pulled out the parts that hold the most relevance to the direction of this discussion, and asked AI to summarize (AI summarizing a convo on AI, gotta love it), and here is what we got:

The rapid development of AI raises major challenges for government adaptation, as existing bureaucratic structures struggle to keep pace with technological change. Some argue that the government itself must be radically restructured to harness AI’s full potential. At the same time, the U.S. is signaling a shift in its regulatory stance, distancing itself from Europe’s more cautious approach to AI governance. Instead of engaging in lengthy multilateral negotiations, the focus is on accelerating AI development while ensuring its integration into the economy benefits workers rather than displacing them.

The impact on labor markets will be profound, though uneven—some industries and firms will be hit first, while others adapt over time. The key challenge will be managing this disruption, ensuring workers have a seat at the table, and using AI to enhance, rather than erode, human potential in the workplace. The next few years will determine whether AI becomes a tool for progress or a force of destabilization.

So to tie this back, Kayla ended her article with the following thoughts:

“Meanwhile, the technological revolution promises productivity gains that could theoretically offset the economic drag from deglobalization. It's not merely a recession, it's a sparkling reconfiguration of the labor market in preparation for an AI-driven economy. The six-to-twelve-month timeline mentioned by the Bessent aligns well with projections for major AI advancements. But - counterarguments and grounding - the CHIPS Act’s cancellation may undercut American leadership in AI hardware, given that advanced semiconductors are critical to training and running large-scale AI models. So. It is murky. The national security dimension of all of this cannot be overlooked. As Buchanan observes: "I do think there are profound economic, military and intelligence capabilities that would be downstream of getting to AGI... And I do think it is fundamental for US national security that we continue to lead in AI."”

In very plain terms, it could be that tariffs and the rest of the administration’s ongoing policy efforts are (among other things) laying the groundwork to create a more productive government, and a more productive US labor force and economy.

Alright, my second rabbit hole that is important to freight: gold. 🪙

You have already seen, and will see, discussions around the surge in imports as a result of a “pull-forward” of goods ahead of tariffs. Yes, this is undeniable. However, it seems that one commodity in particular is majorly skewing with GDP as a result of January’s import levels.

The only economist or article I came across in my research that mentioned this in such detail, is Matthew Klein ’s The Overshoot. Here is what you need to know.

The graph I showed at the beginning of this article showed the really abnormal amount of gold imports into the US in January. Apparently, the US does not usually import more than $1B of gold in any given month. So $28B in one month is definitely an outlier. As it stands, it’s also an outlier that is not accounted for in many economic data trackers. GDP trackers are painting a very negative picture lately, but the reality is that almost all measures of GDP are chugging along just fine. The negative drag has been caused by the surge in import value. Remember that GDP = Consumption + Fixed investment + Changes in inventories + Exports - Imports

While total goods imports jumped 12% from December to January, the increase drops to 6% when excluding gold. This discrepancy has led GDP trackers like GDPNow to project a sharp rise in the goods trade deficit—from $1.3 trillion in Q4 2024 to $1.7 trillion in Q1 2025. However, when gold is stripped out, the deficit increase is much smaller, suggesting a far less severe economic impact than initial estimates indicate. Instead of signaling a downturn, the effect on growth may be more in line with the drag from rising net imports in 2024Q1 and 2024Q2.

Matthew does go on to say -

“All of this said, the desire to get ahead of U.S. tariffs probably did motivate some extra import spending in January. After “finished metal shapes”, the other main contributors to the aggregate increase in imports were pharmaceuticals, computers and parts, and cell phones. But if individuals were buying ahead of tariffs, that spending ought to show up as higher consumer spending. If wholesalers and retailers were buying, then there should be a bump in inventories. Either way, the net effect on quarterly GDP growth should be zero. So far, it is hard to find any evidence of either higher consumer spending or a pop in inventories, but there may be lags between the timing of inventory reporting and trade reporting, or issues with seasonal adjustment.”

Why did we import so much gold? I’m still unsure. You can read the full article for more insights on why we bring gold in from Switzerland that was pulled from London vaults and all the good stuff, but as of right now I have no clear picture on what all this gold was rushed in for. While this topic is one I will likely chase further, I wanted to incorporate it into this report to help us take GDP and Import headlines with a grain of salt (gold?).

Another economic data point worth looking at is the recent jobs data. Jobs data does not align with falling GDP Jan J. J. Groen writes in his recent publication that

“Today’s release of the February Employment Situation report continued to show a labor market with low hirings and low layoffs as well as above-trend hourly wage growth - similar to what we have seen in previous reports. Payrolls growth trends, however, barely can keep up with a still elevated breakeven pace, although the latter should come down later in the year as population growth slows.”

To summarize my key takeaways from the recent jobs data, I’d say that January's jobs data showed payroll growth, but just enough to keep up with population-driven breakeven levels. The unemployment rate rose to 4.1% from 4% as labor force participation declined, while the job-finding rate weakened. Wage growth still remains too high to align with the Fed’s 2% inflation target, creating a mixed outlook: a stable yet fragile labor market alongside rising inflation momentum. As a result, the Fed is likely to stay on hold for now.

I wanted to check in with Jason Miller on manufacturing again this month, as ISM’s PMI data for February was very discouraging. We had just seen some signs of strength in the PMI the last couple months that have now faltered. There was a sharp drop in new orders, and an increase in raw material pricing momentum, which is likely due to increased material costs from tariffs or even just the fear of increased material costs driving up costs preemptively.

At this time, tariffs on the automotive industry have been paused or pushed out at least a couple more weeks. There was just too much to cover in this report without going there, although I suspect it might be a topic I revisit with more focus next month. That said, Jason Miller provided commentary on the weakening motor vehicles sales here in the US.

“February's motor vehicle sales from the Bureau of Economic Analysis suggests that the November and December bump we saw in the seasonally adjusted data wasn't a sustained increase. February's sales came in at ~16 million units on a seasonally adjusted annual rate, which remains about 1 million units below 2017 - 2019 levels. Looking at the types of vehicles, light truck/SUV sales remain slightly above pre-COVID levels, but the ongoing weakness in auto sales is holding total light weight vehicles sales down. Given industrial production in this sector has been slipping, sales remaining stuck below pre-COVID levels isn't encouraging given the tariff situation with Canada and Mexico.”

As I transition into the rate portion of the newsletter, I would advise companies to pay attention to what commodities are likely to be impacted by tariffs regardless of the details of those tariffs. For transportation providers, start to analyze how your manufacturing customers will be impacted by these changes, and start having proactive conversations with them if you identify areas of opportunities that align with your strengths.

For manufacturers, things will stabilize over time (we hope). Years ago when tensions with China started to rise, and tariffs were announced, wheels started turning that have only accelerated with time. In 2023, Mexico displaced China as our largest trading partner. Geopolitical tensions, and tariff policies were some of the primary drivers of that shift. It is likely that when we look back at supply chains in another 4 years, we will see a similar outcome has taken place. I would also urge executives and management to take a good hard look at AI and its application within your business. I think major advancements are likely to take place in the next couple of years, and adoption will be key to maintaining competitive advantages.

A huge thank you to BiggerPicture for sponsoring this month's newsletter! BiggerPicture is focused on helping shippers, brokers, and carriers maximize their operational productivity, by reducing the time spent scheduling appointments by an average of 80%. Achieve full ROI in 3 months or less, and unlock new growth potential by shifting your most valuable resources (your peoples' time) where it can make the biggest impact.

Avery Vise, FTR’s vice president of trucking, commented, “Preliminary data suggests that market conditions were tough for carriers in January, but we still forecast consistently favorable market conditions for carriers to begin soon. Freight rates have been sluggish, however, so the risk of a slower recovery than currently forecast is significant. Volatility in economic data due to tariff expectations and response from businesses and consumers injects further uncertainty into the outlook. Despite these concerns, we are confident in modestly stronger conditions for trucking companies at least by the second half of the year.”

Broker-posted spot market rates in the Truckstop system for dry van and refrigerated equipment returned to their downward trend during the week ended February 28 (week 8) after rising for the first time in six weeks during the prior week. Refrigerated spot rates fell their lowest level since April 2023. Dry van spot rates were at their second lowest level since October. Flatbed spot rates rose to their highest level since late July, and flatbed volume was the strongest since July 2022.

Arrive’s recent market update publication produced by David Spencer and team said:

Volumes remain flat to down as capacity continues to contract, reinforcing the idea that supply, not demand, is driving volatility. While demand trends could move in either direction, it is clear that a low spot rate environment should continue to force capacity exits in the near term, which would increase market vulnerability as the year goes on, particularly if demand levels remain stable or grow. The spot-contract rate gap has closed on a year-over-year basis but remains wide enough to prevent any sustained disruption, meaning an inflationary flip is unlikely unless a black swan event occurs.

Dry van rates have struggled in recent weeks, falling after the seasonal highs of December.

Reefer rates also experienced continued declines falling off of seasonal peaks.

While flatbed rates have been relatively steady there are some signs of some positive momentum building for spring.

And as always, here are the graphs we check on a monthly basis to track spot and contract rate movement in reefer and dry van, thanks to Ken Adamo and team at DAT Freight & Analytics.

As a closing thought, Jason Miller had mentioned this to me:

Though it's way too early to start reading much into DAT's March dry van TL spot estimates, seeing $2.01 per mile today is not encouraging. Likewise, FW's outbound tender rejection index is sub-6 at the moment.

He’s certainly right. We are not yet seeing encouraging movement across the broader truckload market, and tender rejections are still well below 10%, a sign that the market still has ample supply to match current demand.

Meet Me For Coffee with Samantha Jones seeks to correlate macro-economics to freight markets (just like this Newsletter does) and offers a chance to hear various industry and non-industry experts explain their thoughts on economics and freight markets.

Check out our Channels on your preferred platforms!

Thank you so much for reading and supporting the Truckload Market Update Report, produced by Samantha Jones Consulting LLC. Samantha Jones Consulting focuses on helping companies in the logistics industry better brand and sell their services to create sustainable revenue growth, and support their company growth goals!

We love Feedback, if you have questions, comments, suggestions, or are interested in sponsorships or partnerships, please email samantha@connectsjc.com to connect!

Make sure you subscribe to the Newsletter to receive the monthly update, and please share this with a friend who can also benefit from reading! As always, Samantha's work is free and created with the intent to add value to the transportation industry.